Corporate Budgets A Comprehensive Guide

Corporate budgets set the stage for strategic planning and financial success. Understanding these crucial documents is essential for any business. This guide explores the entire process, from initial creation to final evaluation, encompassing various types of budgets, development methods, and external factors that impact their effectiveness.

This document details the intricacies of corporate budgets, covering key elements, different types (operating, capital, master), and the crucial steps in their development and implementation. It also discusses the importance of monitoring and control, performance evaluation, and the role of external factors and effective communication in achieving desired financial outcomes.

Introduction to Corporate Budgets

A corporate budget is a formal financial plan that Artikels anticipated revenues and expenses for a specific period, typically a fiscal year. It serves as a roadmap for the company’s financial activities, guiding resource allocation and ensuring financial stability. It’s more than just a list of numbers; it’s a strategic tool for achieving organizational goals.

Corporate budgets are crucial for strategic planning because they provide a framework for evaluating the feasibility of proposed projects and initiatives. By forecasting potential financial outcomes, businesses can make informed decisions about resource allocation, optimize operational efficiency, and effectively manage risks. This proactive approach enables the organization to adapt to changing market conditions and capitalize on opportunities.

Importance of Corporate Budgets for Strategic Planning

Corporate budgets are integral to strategic planning because they provide a quantitative framework for assessing the financial implications of various strategies. By projecting revenues and expenses, businesses can identify potential bottlenecks and proactively address financial challenges. This forward-looking approach allows for better resource allocation, improved operational efficiency, and enhanced decision-making.

Key Elements of a Corporate Budget

A comprehensive corporate budget typically includes several key elements, ensuring a holistic view of the company’s financial performance. These elements encompass the different aspects of the business, from revenue projections to operational expenses. A well-structured budget considers both short-term and long-term financial goals.

- Revenue Projections: These projections detail anticipated income from various sources, such as sales, investments, and other revenue streams. Accurate revenue projections are essential for aligning resource allocation with anticipated income.

- Expense Budgets: This section Artikels the estimated costs associated with operating the business. Categories include salaries, marketing, rent, utilities, and other operational expenses. Proper expense budgeting helps maintain financial control and prevents overspending.

- Capital Expenditure (CapEx) Budget: This segment Artikels planned investments in fixed assets, such as property, plant, and equipment. These investments are crucial for long-term growth and expansion, impacting the company’s overall financial health.

- Cash Flow Projections: These projections illustrate the expected inflows and outflows of cash over the budget period. Cash flow management is critical for ensuring the company has sufficient liquidity to meet its short-term obligations.

- Profit and Loss (P&L) Statement: This statement summarizes the projected revenues and expenses, highlighting the expected profit or loss for the budget period. This provides a concise overview of the company’s financial performance.

Corporate Budget Template Example

The following table provides a simplified example of a corporate budget template for a hypothetical software company.

| Category | Q1 2024 | Q2 2024 | Q3 2024 | Q4 2024 |

|---|---|---|---|---|

| Revenue (Sales) | $50,000 | $60,000 | $70,000 | $80,000 |

| Cost of Goods Sold (COGS) | $15,000 | $18,000 | $21,000 | $24,000 |

| Operating Expenses | $10,000 | $12,000 | $14,000 | $16,000 |

| Profit Before Tax | $25,000 | $30,000 | $35,000 | $40,000 |

| Tax | $5,000 | $6,000 | $7,000 | $8,000 |

| Net Profit | $20,000 | $24,000 | $28,000 | $32,000 |

Budget Development Process: Corporate Budgets

The corporate budget is not a static document; it’s a dynamic tool reflecting the company’s strategic objectives and operational realities. A well-defined budget development process ensures alignment between departmental goals and overall corporate strategy. This process requires meticulous planning, collaboration, and a clear understanding of the company’s financial position and future outlook.

Developing a comprehensive budget involves multiple stages, each with distinct roles and responsibilities. Accurate forecasting is paramount, allowing for adjustments based on market conditions and internal performance. This iterative process ensures the budget is not just a financial projection, but a living document capable of adapting to changing circumstances.

Stages of Budget Creation

The budget development process typically unfolds through several key stages. Each stage builds upon the previous one, ensuring a consistent and comprehensive approach to budget creation. This process emphasizes collaboration between departments and fosters a shared understanding of the budget’s importance.

- Strategic Planning & Goal Setting: This initial stage focuses on aligning departmental objectives with the overall corporate strategy. The company’s long-term goals and short-term objectives are clearly defined, and specific targets are established for each department. This stage sets the foundation for the entire budget process.

- Data Collection & Analysis: Data collection is crucial for accurate forecasting and budgeting. This involves gathering historical financial data, market research, industry trends, and anticipated changes in operational costs. Detailed analysis of this data provides insights into potential challenges and opportunities.

- Departmental Budget Preparation: Each department prepares its individual budget proposal, outlining anticipated revenues, expenses, and resource requirements. This requires a thorough understanding of the department’s operations and future plans. The budget should align with the overall corporate strategy and departmental objectives.

- Coordination & Review: The individual departmental budgets are reviewed and coordinated by the finance department. This process ensures consistency across departments and alignment with the overall corporate budget. Potential conflicts or inconsistencies are identified and resolved during this stage.

- Approval & Finalization: The finalized budget is reviewed and approved by senior management. This process involves considering the budget’s impact on the company’s financial health and strategic goals. Once approved, the budget is documented and disseminated to relevant parties.

Roles & Responsibilities

Different departments play crucial roles in the budget development process. Clear definition of responsibilities ensures accountability and effective collaboration. This collaborative approach fosters a sense of shared ownership and commitment to the budget’s success.

| Department | Role |

|---|---|

| Finance | Oversees the entire process, coordinates departmental budgets, and ensures compliance with financial policies. |

| Marketing | Provides market analysis and revenue projections based on market research and sales forecasts. |

| Operations | Provides detailed cost estimates for production, materials, and labor. |

| Sales | Develops sales forecasts and revenue projections, considering market trends and competitor activities. |

| Human Resources | Provides staffing requirements and associated costs based on anticipated workload and growth projections. |

Importance of Accurate Forecasting

Accurate forecasting is essential for developing a realistic and effective budget. A reliable forecast enables informed decision-making and proactive adjustments to changing market conditions. Inaccurate forecasts can lead to financial mismanagement and strategic misalignment.

Step-by-Step Departmental Budget Development

A structured approach to departmental budgeting ensures consistency and accuracy. A well-defined process streamlines the budget development process and promotes clarity within the department.

- Define Objectives: Clearly articulate the department’s objectives and goals for the upcoming fiscal period. These objectives should align with the overall corporate strategy.

- Gather Historical Data: Compile relevant financial data from previous periods, including revenue, expenses, and resource utilization. Analyze trends and identify areas for improvement or potential risks.

- Project Revenue & Expenses: Project anticipated revenue based on sales forecasts and market analysis. Estimate expenses based on anticipated resource utilization, material costs, and labor requirements.

- Review & Adjust: Carefully review the proposed budget for accuracy and alignment with departmental objectives. Make necessary adjustments based on insights from market analysis and internal performance.

- Submit to Finance: Submit the finalized departmental budget to the finance department for coordination and review.

Budget Implementation and Control

Implementing and controlling a corporate budget is a critical aspect of financial management. Effective implementation ensures the budget aligns with strategic goals, while robust control mechanisms guarantee accountability and identify potential deviations. This section explores the methods used to execute budgets, the monitoring and control procedures, and the pivotal role of variance analysis in maintaining budgetary integrity.

Budget implementation hinges on clear communication and a well-defined process. A robust communication strategy, outlining roles and responsibilities, helps ensure all departments understand and adhere to the budget guidelines. This, in turn, promotes coordinated efforts towards achieving the organizational objectives.

Budget Implementation Methods

Different methods exist for implementing budgets, tailored to the specific organizational structure and industry. These methods often include direct allocation of funds to departments, project-based budgeting, or a combination of these approaches. Effective budget implementation is crucial for fostering a culture of accountability and ensuring financial discipline.

Budget Monitoring and Control

Regular monitoring of budget performance is essential for maintaining control. This entails comparing actual expenses against planned expenditures on a regular basis, usually monthly or quarterly. Key performance indicators (KPIs) can be instrumental in tracking progress and identifying areas where adjustments are needed. Tools such as dashboards and reporting systems can facilitate this process, enabling real-time insights into budget performance. For example, if a department consistently exceeds its allocated marketing budget, it signals a need for revised strategies or more rigorous cost controls.

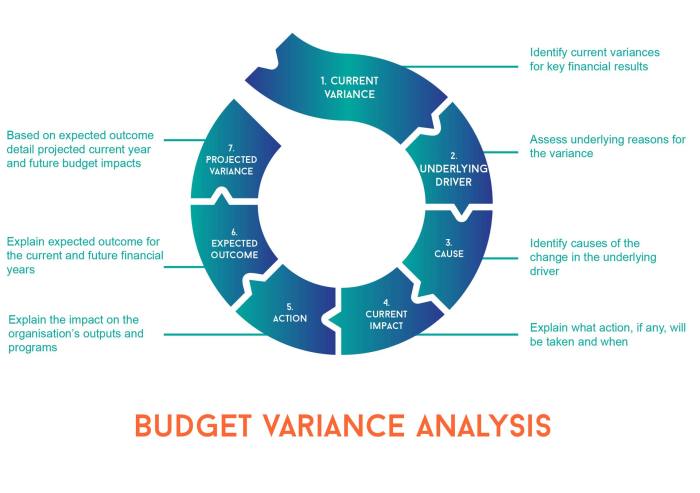

Variance Analysis

Variance analysis is a crucial component of budget control. It identifies discrepancies between planned and actual results. By analyzing variances, management can pinpoint areas needing attention and make necessary adjustments to stay on track. Understanding the reasons behind variances is essential to addressing them effectively. For instance, a significant increase in raw material costs might warrant a review of supply chain strategies or exploring alternative suppliers.

Variance analysis is the process of identifying and investigating the difference between planned and actual results.

Common Budget Variances and Potential Causes

| Variance Type | Potential Causes |

|---|---|

| Favorable Revenue Variance | Higher-than-expected sales, improved pricing strategies, increased market share |

| Unfavorable Revenue Variance | Lower-than-expected sales, pricing pressure, decreased market share |

| Favorable Cost Variance | Lower-than-expected material costs, improved efficiency, cost-cutting initiatives |

| Unfavorable Cost Variance | Higher-than-expected material costs, inefficiencies in production, increased labor costs |

| Favorable Expense Variance | Reduced marketing costs, lower administrative expenses, better negotiation of contracts |

| Unfavorable Expense Variance | Increased marketing expenses, higher administrative expenses, unexpected contractual obligations |

Budgetary Performance Evaluation

Evaluating budgetary performance is crucial for a company’s financial health and strategic decision-making. It allows for identifying areas of strength and weakness, adjusting strategies, and ensuring resources are allocated effectively. Understanding how well the budget is being followed enables proactive problem-solving and fosters a culture of accountability.

Key Performance Indicators (KPIs)

A range of KPIs are used to assess budgetary performance. These metrics provide a comprehensive view of the financial health of the organization. They allow for a comparative analysis of planned vs. actual results, enabling the identification of potential issues and opportunities.

- Revenue Growth: This KPI tracks the actual revenue generated against the budgeted revenue. Significant deviations can indicate market shifts, pricing strategies, or sales team effectiveness needing adjustments.

- Cost Variance: This metric compares actual costs to budgeted costs for various categories like materials, labor, and overhead. Analyzing variances helps pinpoint cost overruns or efficiencies. Understanding cost drivers is essential in this analysis.

- Profitability: This KPI assesses the difference between actual revenue and actual costs. Comparing this against the budgeted profit reveals profitability trends and helps evaluate the overall financial performance.

- Efficiency Ratios: These ratios, such as the number of sales per employee or cost per unit, evaluate operational effectiveness. Deviations from planned efficiency ratios often pinpoint areas needing process improvement.

- Cash Flow: This KPI tracks the actual cash inflows and outflows against the budgeted cash flow. Maintaining a healthy cash flow is critical for meeting obligations and ensuring business continuity.

Analyzing Budget Variances

Budget variances represent the difference between planned and actual figures. A systematic analysis of these variances is essential for understanding the reasons behind them. This involves a thorough investigation into the underlying causes, from market changes to operational inefficiencies.

- Identify the Variance: The first step involves recognizing the difference between the budgeted amount and the actual result for each category.

- Analyze the Cause: This step involves understanding the factors that contributed to the variance. This could include market conditions, pricing changes, or unexpected operational costs.

- Develop Corrective Actions: Based on the analysis, appropriate corrective actions are implemented to address the identified causes. This could involve adjusting strategies, improving efficiency, or seeking alternative solutions.

Management’s Role in Responding to Variances

Management plays a critical role in responding to budget variances. This involves a proactive approach to understanding the reasons behind deviations and implementing necessary changes. Their oversight ensures that the organization adapts to market conditions and operational issues in a timely and efficient manner. Furthermore, they should ensure that any necessary changes in the budget are communicated effectively.

KPI Comparison Table

| KPI | Description | Example Calculation | Interpretation |

|---|---|---|---|

| Revenue Growth | Actual Revenue / Budgeted Revenue | $10,000,000 / $9,000,000 = 1.11 | 11.1% growth; potentially exceeding expectations. |

| Cost Variance | Actual Cost – Budgeted Cost | $5,000,000 – $4,500,000 = $500,000 | $500,000 cost overrun; investigate reasons. |

| Profitability | Actual Revenue – Actual Costs | $10,000,000 – $5,000,000 = $5,000,000 | Profit exceeds budget; maintain this momentum. |

| Efficiency Ratios | Sales per Employee or Cost per Unit | $1,000,000 Sales / 50 Employees = $20,000 per employee | Efficiency is strong compared to budget; maintain. |

| Cash Flow | Actual Cash Inflow – Actual Cash Outflow | $2,000,000 Inflow – $1,500,000 Outflow = $500,000 | Positive cash flow; manage resources efficiently. |

Budgetary Tools and Techniques

Effective budgeting relies on a variety of tools and techniques to ensure accuracy, efficiency, and alignment with strategic goals. These tools allow businesses to allocate resources effectively, track progress, and make informed adjustments throughout the fiscal year. Different approaches cater to various organizational structures and needs.

Budgeting Techniques

Various budgeting techniques exist, each with its own strengths and weaknesses. Understanding these approaches allows businesses to select the most suitable method for their specific circumstances.

- Zero-Based Budgeting: This approach requires justifying every expense from a zero base, meaning each budget item must be justified individually. This technique forces a critical evaluation of spending and encourages managers to scrutinize the necessity of each activity. By starting from scratch, organizations can identify unnecessary costs and potentially reduce spending. For example, a department might demonstrate that certain equipment is obsolete and can be replaced with more efficient alternatives.

- Activity-Based Budgeting: Activity-based budgeting (ABB) focuses on the activities required to achieve organizational objectives. It identifies the cost drivers behind each activity and allocates resources based on these drivers. This method offers a more detailed understanding of cost behavior than traditional methods. For example, a marketing department might allocate more budget to social media campaigns based on the increased engagement and conversion rates observed in these activities compared to traditional print advertising.

- Incremental Budgeting: Incremental budgeting builds upon the previous budget by adding or subtracting amounts to the prior year’s figures. This method is often easier and quicker to implement, as it leverages existing data. However, it may not fully reflect changing circumstances or strategic priorities.

Benefits and Drawbacks of Budgeting Approaches

Each budgeting approach offers distinct advantages and disadvantages. A careful evaluation of these factors is crucial in selecting the optimal method.

| Budgeting Approach | Benefits | Drawbacks |

|---|---|---|

| Zero-Based Budgeting | Forces thorough justification of all expenses, promotes efficiency, reduces waste. | Time-consuming, complex, can be overwhelming for large organizations. |

| Activity-Based Budgeting | Provides a detailed understanding of cost drivers, improves resource allocation, promotes cost control. | Requires significant data collection and analysis, implementation can be complex and costly. |

| Incremental Budgeting | Relatively simple and quick to implement, leverages existing data. | May not reflect changing circumstances, doesn’t encourage cost-cutting measures, risks perpetuating inefficiencies. |

Technology in Budget Processes

Technology plays a vital role in streamlining and enhancing budget processes. Modern software solutions automate tasks, provide real-time data analysis, and facilitate collaboration.

- Automated Data Collection: Software can automate the collection of data from various sources, reducing manual effort and improving accuracy. This integration reduces the risk of errors associated with manual data entry.

- Real-Time Reporting: Real-time budget reporting tools provide up-to-the-minute insights into financial performance, enabling managers to identify deviations from plans and make timely adjustments. This allows for swift and effective corrective actions, which might include reallocating resources based on actual performance.

- Collaboration and Communication: Budgeting software facilitates collaboration among different departments and stakeholders, promoting transparency and alignment on financial goals. It also improves communication through dashboards and reports, making it easier to share budget information with relevant parties.

Budgeting Software Example: [Software Name]

[Software Name] is a comprehensive budgeting software solution designed to support organizations in various stages of the budgeting process. Its features and benefits make it a valuable asset for companies of all sizes.

- User-Friendly Interface: The intuitive interface simplifies navigation and data entry, reducing the learning curve for users. This feature makes it easier for non-financial professionals to understand and utilize the software.

- Data Integration: The software integrates with various accounting systems, ensuring data consistency and reducing manual data entry. This seamless data flow minimizes data discrepancies.

- Customizable Reports: The software allows users to customize reports and dashboards, providing tailored insights into budget performance. This tailored approach is crucial for gaining a precise understanding of the company’s financial health.

- Automated Forecasting: Automated forecasting capabilities help predict future financial trends, enabling proactive planning and decision-making. This feature assists in making better informed decisions and anticipates potential issues.

Budget Communication and Transparency

Effective budget communication is crucial for aligning stakeholders with organizational goals and fostering trust. Open and clear communication about budget plans, performance, and any deviations promotes understanding and facilitates collaboration. Transparency in the budget process builds confidence among employees, investors, and the public.

Importance of Effective Budget Communication

Clear communication of the budget ensures everyone understands the financial plan, its implications, and their roles in achieving its objectives. This clarity fosters buy-in and reduces misunderstandings, potentially leading to improved performance and increased efficiency. Moreover, well-communicated budgets help manage expectations, anticipate potential challenges, and facilitate proactive adjustments.

Methods for Communicating Budgets to Stakeholders

Several methods facilitate budget communication to diverse stakeholders. Regular updates via presentations, reports, and newsletters keep key personnel informed about budget progress and any critical developments. Interactive workshops and Q&A sessions provide platforms for stakeholders to ask questions and gain clarity on budget allocations. For wider dissemination, easily accessible online dashboards and summary reports make budget information readily available.

Role of Transparency in Budget Processes

Transparency is essential in budget processes to cultivate trust and accountability. Openly sharing budget data, rationale behind decisions, and performance metrics builds confidence and encourages scrutiny, thereby mitigating potential risks and ensuring fairness. This approach fosters a culture of responsibility, encourages participation, and promotes a shared understanding of financial objectives. Transparent budget processes are more likely to gain acceptance and support from all stakeholders.

Example of a Clear and Concise Budget Summary Report, Corporate budgets

Category 2024 Budget (USD) 2023 Actual (USD) Variance Personnel 1,200,000 1,150,000 +50,000 (5%) Marketing 300,000 280,000 +20,000 (7%) Technology 400,000 380,000 +20,000 (5%) Total 1,900,000 1,810,000 +90,000 (5%)

This concise summary report clearly presents key budget figures, allowing stakeholders to quickly grasp the financial overview and identify any notable variances between the projected and actual figures. The inclusion of variance highlights potential areas requiring attention.

Best Practices for Effective Budgeting

Source: com.au

Effective corporate budgeting is crucial for strategic planning and financial stability. A well-structured budget provides a roadmap for resource allocation, performance measurement, and informed decision-making. Adhering to best practices ensures alignment with organizational goals and facilitates the achievement of desired outcomes.

Implementing a robust budgeting process requires a multifaceted approach, encompassing clear communication, thorough analysis, and continuous improvement. This encompasses not just the creation of the budget but also its subsequent monitoring and adaptation to changing circumstances. A robust budget system fosters accountability and transparency throughout the organization.

Key Best Practices for Budget Development

A robust budget development process hinges on several key practices. These include meticulous data collection, rigorous analysis, and collaborative input from relevant stakeholders. Clear communication channels and established timelines are paramount to ensure smooth execution. This process should be standardized and consistently applied across departments to maintain consistency and accuracy.

- Data-Driven Analysis: Utilizing historical data, market trends, and internal performance indicators is essential for creating realistic and accurate budgets. Forecasting models and scenario planning tools can be employed to evaluate potential outcomes under different circumstances. Accurate data informs prudent allocation of resources.

- Stakeholder Collaboration: Involving all relevant stakeholders in the budget process fosters buy-in and ensures that the budget reflects the needs and priorities of different departments and functions. Open dialogue and active listening are crucial for creating a shared understanding and a sense of ownership.

- Clear Communication and Transparency: The budget should be communicated clearly and transparently to all stakeholders. This includes providing a comprehensive explanation of the budget’s rationale, assumptions, and potential implications. This ensures that everyone understands the financial direction of the company.

- Well-Defined Timelines: Establishing clear timelines and deadlines for each stage of the budget process is critical. This helps to maintain momentum, prevent delays, and ensure that the budget is finalized in a timely manner. Strict adherence to deadlines keeps the budget process on track.

Continuous Improvement in Budgeting

Continuous improvement in the budgeting process is essential for optimizing resource allocation and achieving organizational goals. This iterative approach allows for adjustments based on performance data and emerging trends. Regular review and analysis of the budget’s effectiveness can enhance its accuracy and relevance.

- Post-Budget Analysis: Regularly evaluating the budget’s performance against actual results is vital. Identifying variances and their root causes allows for proactive adjustments and course correction. This analysis helps identify areas for improvement in future budgeting cycles.

- Feedback Mechanisms: Implementing robust feedback mechanisms enables continuous improvement. Gathering feedback from stakeholders about the budget process allows for adjustments to be made to future budgets. This can help to refine the process for greater efficiency and accuracy.

- Benchmarking: Comparing the organization’s budgeting practices to industry best practices and those of successful competitors can reveal areas where improvements can be made. This benchmarking process provides valuable insights and helps to identify best practices in the industry.

Successful Budgeting Case Study: XYZ Corporation

XYZ Corporation successfully implemented a new budgeting process that significantly improved their financial performance. The key strategies included:

- Collaborative Budgeting: All departments participated in the budgeting process, fostering a shared understanding of organizational goals and contributing to a more accurate reflection of departmental needs.

- Data-Driven Forecasting: XYZ Corporation employed sophisticated forecasting models based on historical data and market research. This enhanced the accuracy of their budget projections.

- Performance-Based Incentives: The new budget process incorporated performance-based incentives, aligning individual and departmental goals with organizational objectives. This encouraged proactive participation and adherence to budget targets.

The results were substantial. XYZ Corporation achieved a 15% increase in profitability within the first year of implementing the new budgeting process, demonstrating the significant impact of a well-structured and collaborative approach to budgeting.

Final Conclusion

In conclusion, corporate budgeting is a dynamic process requiring careful planning, implementation, and evaluation. Successfully navigating the complexities of budgeting necessitates a deep understanding of the various types, the development process, and the crucial role of external factors. By implementing best practices and embracing continuous improvement, organizations can leverage their budgets to achieve financial goals and drive long-term success.